Getting pre-approved for a home loan is a crucial step in the home buying process, as it gives you a clear idea of your budget and shows sellers you’re a serious buyer. While it’s not a guaranteed loan offer, it’s a conditional commitment from a lender to lend you a specific amount of money. Here are the essential steps to get pre-approved for a home loan.

- Understand the difference between pre-qualification and pre-approval: Pre-qualification is an early estimate of what you might be able to borrow, based on information you provide and a credit check. Pre-approval is a more formal process where the lender verifies your financial information and performs a credit check, providing you with a letter stating the specific amount you’re approved for.

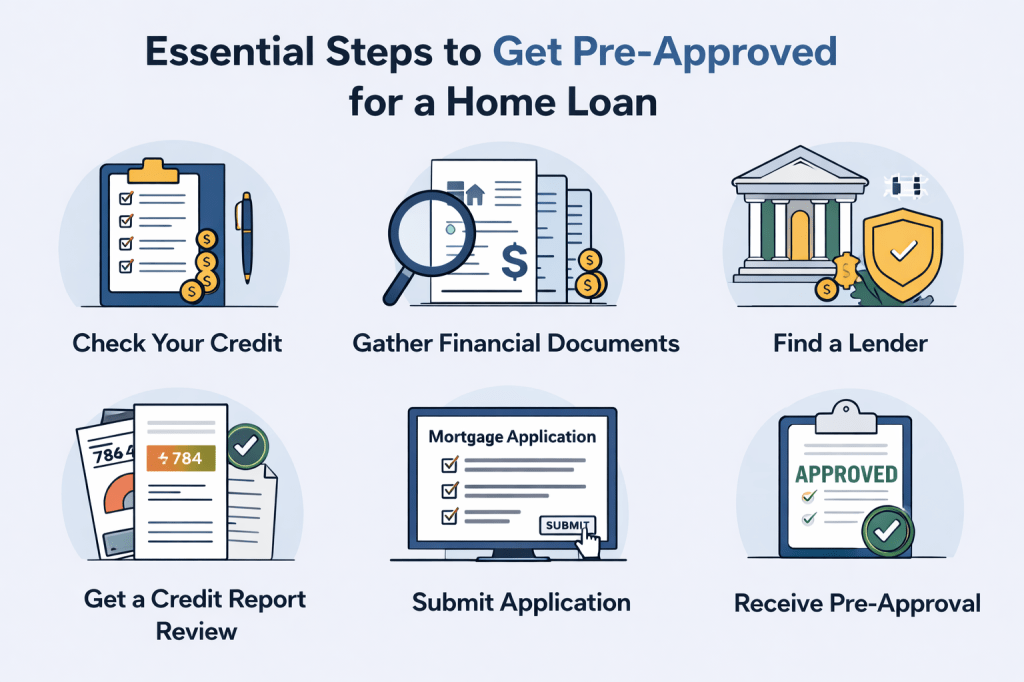

- Choose your lender: Research different mortgage lenders, including banks, credit unions, and online lenders. Compare their rates, fees, and customer service reviews. You can obtain pre-approval from multiple lenders to find the best terms.

- Submit an application: Once you’ve chosen a lender, you’ll need to complete a mortgage application. Be prepared to provide detailed information about your financial situation, including your personal ID (like a driver’s license and Social Security number), proof of income (pay stubs, W-2s, tax returns), employment verification, bank statements, and a list of your assets and debts. The lender will also pull your credit report.

- Await review: The lender will evaluate your financial documents and creditworthiness. This process can take anywhere from a few days to about 10 business days after you’ve provided all requested information. During this time, it’s wise to avoid making large purchases or opening new credit lines, as these could impact your credit score and debt-to-income ratio.

- Receive your pre-approval letter: If everything checks out, you’ll receive a pre-approval letter. This letter indicates the maximum amount the lender is tentatively willing to lend you and usually has an expiration date, typically between 60 and 90 days. This letter is a powerful tool when making an offer on a home, as it demonstrates to sellers that you’re a serious buyer with the financial means to complete the purchase.

All in all, getting pre-approved isn’t just a box to check—it’s the moment your home search becomes real. It gives you clarity, confidence, and leverage before emotions ever enter the picture. When you take this step early and do it the right way, you stop guessing and start moving with intention. And when you’re ready to turn that approval into a smart, well-timed purchase, having the right plan—and the right guide—makes all the difference.

Leave a comment