Owning a primary residence can come with several valuable tax benefits that can help offset the costs of homeownership. These benefits generally apply if you itemize your deductions on your federal income tax return. Here are some of the key tax advantages

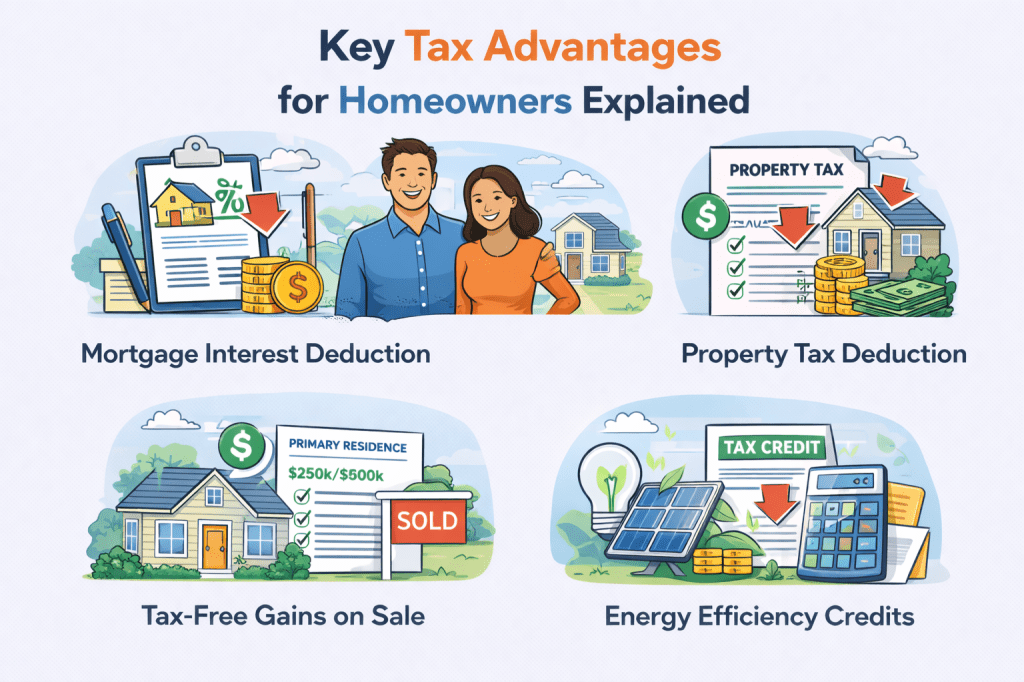

- Mortgage Interest Deduction – You can typically deduct the interest paid on your home mortgage. This applies to mortgages used to buy, build, or substantially improve your primary residence. For most loans taken out after December 16, 2017, you can deduct interest on up to $750,000 of mortgage debt. For loans established before this date, the limit is $1 million. This deduction can also apply to interest on home equity loans or lines of credit (HELOCs) if the funds are used for significant home improvements.

- Property Tax Deduction – Homeowners can deduct state and local real estate taxes, also known as property taxes, from their federal taxable income. However, there’s a limit to this deduction: you can deduct up to $10,000 for state and local taxes (SALT), which includes property taxes and your choice of income or sales taxes.

- Capital Gains Exclusion – When you sell your primary residence, you might be able to exclude a significant portion of the profit (capital gain) from your taxable income. If you’re single, you can exclude up to $250,000 in profits, and married couples filing jointly can exclude up to $500,000. To qualify for the full exclusion, you must have owned the home and used it as your primary residence for at least two of the five years before the sale.

- Exclusion of Imputed Rental Income – One often overlooked benefit is that the “imputed rental income”—the value of living in your own home rent-free—is not taxed. While landlords must report rental income, homeowners don’t have to count the rental value of their own home as taxable income.

- Mortgage Interest Credit – For lower-income individuals, the Mortgage Interest Credit can provide additional assistance. If you qualify and were issued a Mortgage Credit Certificate by your state or local government for a new mortgage on your main home, you can claim a credit each year for part of the home mortgage interest paid.

- Deductions for Ministers and Military Personnel – Ministers and members of the uniformed services who receive a nontaxable housing allowance can still deduct their real estate taxes and home mortgage interest without having to reduce their deductions based on that allowance. It’s important to remember that most of these tax benefits require you to itemize your deductions, which means your total itemized deductions must be greater than the standard deduction you’re eligible for. Also, certain costs like homeowner’s insurance, principal mortgage payments, utilities, and homeowners’ association fees are generally not deductible. Always consult with a qualified tax professional to understand how these benefits apply to your specific financial situation.

Real estate decisions are rarely just about the sale itself, they’re about timing, preparation, and how each choice fits into the bigger picture. My role is to help you understand how today’s market conditions, pricing strategy, and next steps align with your long-term goals, so you’re not just making a move—you’re making the right one.

Leave a comment